Blockchain

India embraces B-side of Bitcoin space, while discarding cryptocurrency itself

“I have heard of an advice around in the startup circle. To increase your venture capital or VC funding by 10%, tell investors you run a ‘platform,’ not a regular business. If you want to increase your funding by 20%, tell investors that you are operating in the ‘fintech space’. But if you really want the investors to empty their pockets, tell them that you are using ‘blockchain” ~ Prime Minister of India, Narendra Modi.

The Blockchain Fever

Blockchain technology – a native language for those in the space and a foreign language for those outside. Nevertheless, the sentiment for blockchain has always been bullish as everyone wants to buy into a technology that “solves it all.”

When Bitcoin soared to its highest valuation towards the end of 2017, it was also the beginning of blockchain mania. Everyone wanted to buy in on the technology, from start-ups to conglomerate companies to banks and governments; they all wanted to jump on board the ship that would take them ‘to the moon.’

The hype built was so much so that existing companies started to rebrand their names with either “blockchain” or “Bitcoin” in it. The companies that did, saw a massive surge in their stock prices during the crypto-craze.

However, when the Bitcoin bubble burst with the price of the cryptocurrency seeing a slump of over 80 percent from its all-time high, even though the ICO mania registered lower tones of exuberance, Blockchain technology was here to stay!

Even now, several private and public sectors are implementing blockchain to test out its promising use cases, with governments taking the lead.

It’s about the tech, not the cryptocurrency

“Disruptive technologies such as Block-chain and the Internet of Things, will have a profound impact in the way we live and work. They will require rapid adaptation in our workplaces” ~ PM Narendra Modi.

Indian regulatory authorities’ pessimistic view of Bitcoin and other cryptocurrencies is no new tale to tell. However, their view on blockchain, on the contrary, is a completely different story. State governments are racing to be on top of the blockchain game, from providing incentives to enterprises and start-ups to establishing training centers, making blockchain technology the flavor of the season.

On Blockchain’s potential in India, Sidharth Sogani, CEO of CREBACO, told AMBCrypto,

“In India, blockchain space is a car without a driver. We see the prime minister talking about blockchain because this is a hyped technology […] India has tremendous growth potential with estimated market size of 12.9Billion USD and the possibility of creating over 20000 Jobs in the very first year of regulation. India has the best tech developers who are still handcuffed from venturing into the crypto and blockchain space in my opinion”

In India, blockchain space is a car without a driver. We see the prime minister talking about blockchain because this is a hyped technology.

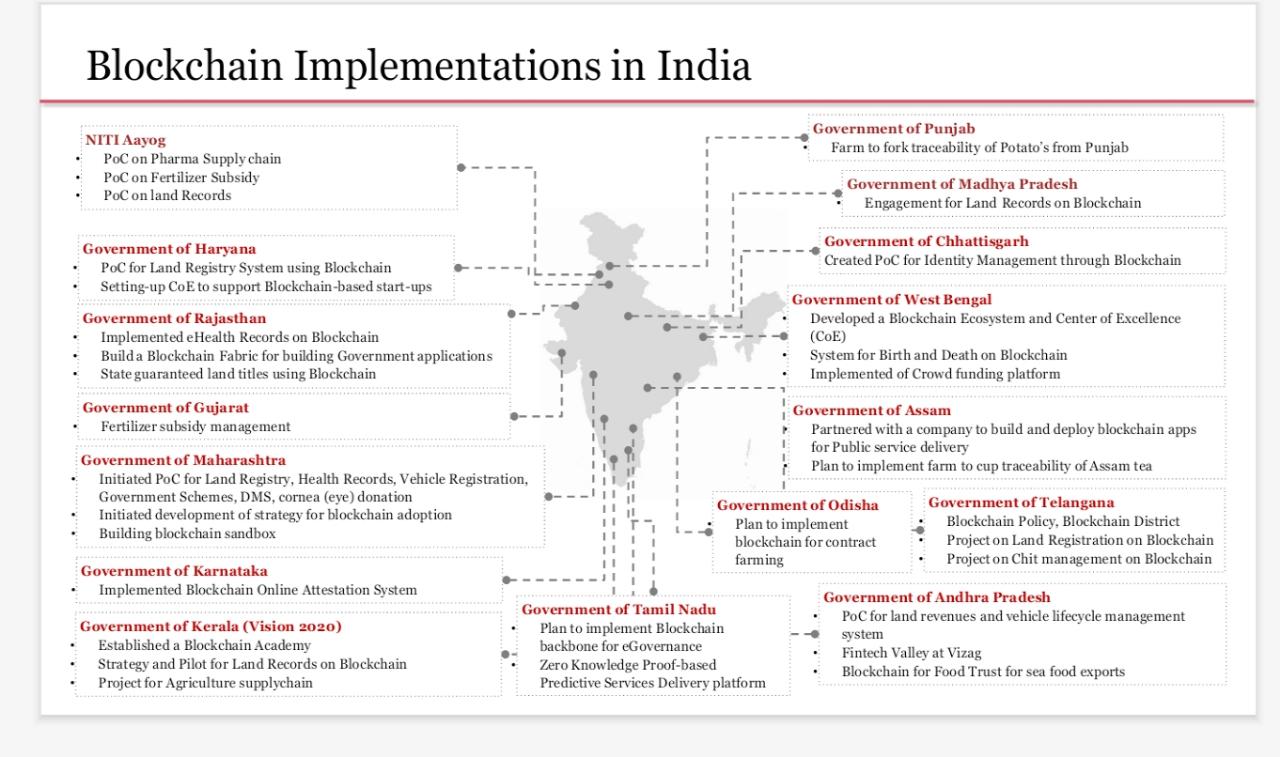

Blockchain Implementation in India | Source: Varun | Blockchain Lawyer India

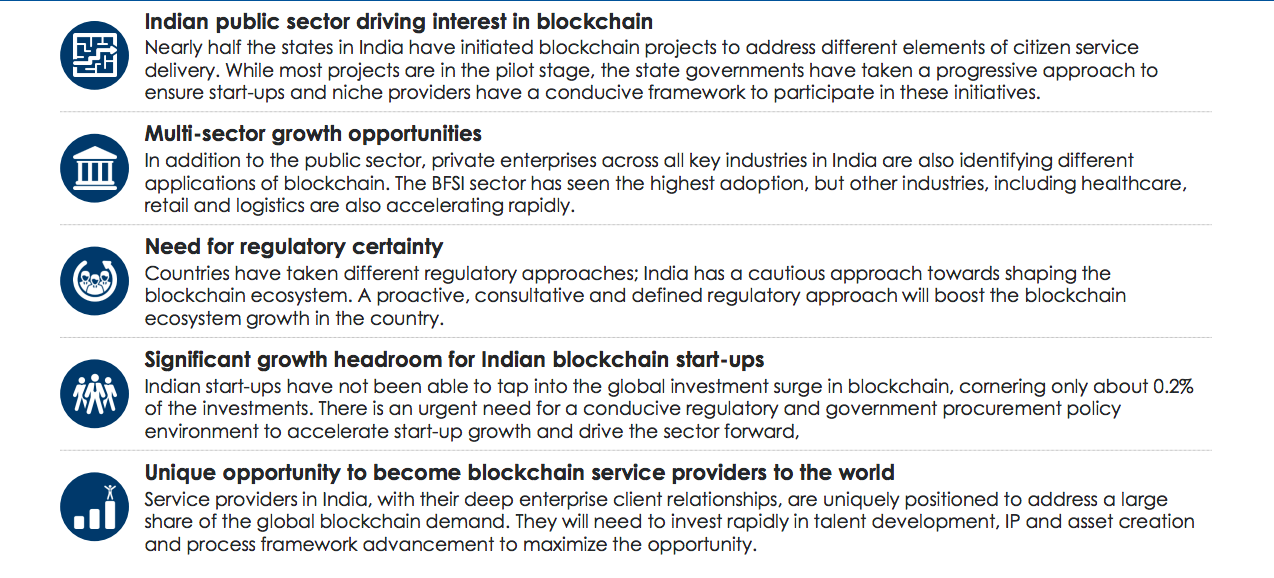

A report by NASSCOM titled ‘Indian Blockchain Report 2019’ stated that “nearly half the states in India have initiated blockchain projects to address different elements of citizen service delivery.” The leading use cases the technology is being leveraged for are land registry, farm insurance, and digital certificates.

Source: NASSCOM

Presently, Telangana and Andra Pradesh, the two states that were once united, are head to head in the blockchain game, with AP pushing Vizag with the “Fintech Valley Vizag Initiative” and Telangana nurturing Hyderabad in its blockchain policy draft that was released earlier this year.

On Telangana and Andra Pradesh stepping into the blockchain space, Sidharth Sogani said,

“The Andra Pradesh and Telangana governments claim to have a Blockchain, but it’s a centralized blockchain which doesn’t really solve the purpose. The data hence is not immutable. They have done few pilot projects to put land and other governments record on blockchain-based certificates, but its easy and even a 15-year-old can do it. To do it in the right manner governments should first Regulate Research Educate And only then Invest.”

The most common use cases of blockchain in India’s public sector are,

- Land title registry

- Vehicle lifecycle management

- Citizen electronic health record management

- Organ tracking for transplant

- Digital certificates

- Benefits distribution

- Rationing

- E-governance

- Benefit distribution

- Chit fund operations administration

- Farm insurance

- Microfinance for self-help groups

- Identity management

- Power distribution

- Cybersecurity

- Duty payments

- Agriculture supply chain

Interestingly, the emerging technology could also make its debut in India’s defense sector. The Defense Minister of India, Rajnath Singh, had stated,

“The role of AI, big data, and blockchain technology has already revolutionized that existing paradigm of warfighting. The defense industry is undergoing a churning to cope and employ these technologies, in order to safeguard the safety and security of critical infrastructure.”

Indian Banks Venture

While state governing bodies are head-to-head in the blockchain game, other sectors are not particularly shying away from the new disruptive technology either. The banking sector in India has emerged as one of the leading sectors in India to leverage the technology for testing faster cross-border transactions and trade settlements.

On one hand, the Reserve Bank of India has time and again scoffed over the idea of cryptocurrencies; on the other hand, India’s central bank has also embraced its underlying technology. These financial institutions are directly collaborating with leading fintech firms in the cryptocurrency space to test out the use cases of blockchain, with Ripple standing out in the country.

Interestingly, the RBI itself has launched a blockchain initiative for banking purposes under its research and development branch, Institute for Development and Research in Banking Technology [IDRBT]. The central bank will reportedly be launching blockchain applications this coming year.

The biggest Indian private banks that are also partaking in blockchain mania are Federal Bank, Kotak Mahindra Bank, ICICI Bank, and HDFC Bank. Other banks that are active in this sector include South Indian Bank, Bank of Baroda, State Bank of India, and Induslnd Bank.

Finance Secretary Subhash Chandra Garg also acknowledged the use cases presented by distributed ledger technology. Garg said,

“The DLT-based systems can be used by banks and other financial firms for processes such as loan-issuance tracking, collateral management, fraud detection, and claims management in insurance and reconciliation systems in the securities market”

Indian Companies Venture

Even major companies such as Bajaj Group, Tata Consultancy Services, and Reliance Industries Limited, India’s multinational conglomerates, have announced that they would be venturing into the blockchain space to provide better services. Reliance Industries’ CEO Mukesh Ambani unveiled the company’s blockchain venture during its 42nd Annual General Meeting [AGM].

Ambani stated that blockchain technology would be leveraged to “invent a brand-new model for data privacy,” while emphasizing that Indian users’ data will be “owned and controlled by the Indian people and not by corporates, especially global corporations.”

In August 2019, Mukesh Ambani, Managing Director of Reliance Industries Limited, added,

“Data is wealth and Indian wealth must remain in India. Over the next 12 months, Jio will install across India one of the largest blockchain networks in the world with tens of thousands of nodes operational on a daily basis”

While Ambani’s ambitions of Blockchain India is big, Sogani asserted that the dream would be fulfilled only if there was a token on top of it. He said,

“In my opinion, a blockchain with 10000 public nodes cannot function without a reward or a token on top. Hence, we may see crypto regulations soon, thanks to Mr.Ambani.”

Vincent Poon, VP of Bithumb, also spoke about India’s blockchain space in an interview with AMBCrypto. The South Korean-based cryptocurrency exchange recently announced its venture into India’s crypto-space, with the promise of being regulated if the regulatory environment is favorable. Additionally, the exchange also announced plans for partnering with blockchain-based startups and companies.

He stated,

“India is one of the most important regions for us. I have traveled to a lot of places and noticed that there was a huge developer base in India […] We’re more towards empowering the whole ecosystem, the crypto-to-crypto, the blockchain projects, incubating projects, and blockchain integrating projects. “

Futuristic View

While China and the USA are debating over who’s going to be the next tech supreme, India’s following close behind too. Moreover, a 2018 survey by PWC projected India to be among the top five blockchain leaders for 2021-2023, falling behind only China, the United States, and Australia.

*Updated with quotes from Sidharth Sogani