Ethereum

Here’s why ETHUSD Perpetual swaps can do better

Many times, perpetual markets have outpaced spot markets for a multitude of reasons. High leverage is the primary driver of growth. It brings in new buyers and traders. Traders look for options like margining in crypto instead of fiat, and no expiry, as opposed to dated futures. This makes perpetual swap lucrative. To top this off, it is the easiest derivative product to short. They are used for tracking demand and price movement of the underlying asset.

Contracts with fixed expiry dates require a trader to sell or buy the underlying asset within a stipulated time frame and this anchors futures contracts to spot prices. However, perpetual contract prices may deviate +- 0.5% from spot prices due to the underlying mechanism – funding rate.

When the perpetual swap price is higher than the index price, shorts are paid for by positive funding to encourage the price and bring it closer to the index. This may have a short-term negative impact on the demand for longs. The demand for shorts consequently shoots up, until the perpetual price is closest to the index. Similarly, when the perpetual swap price is lower than the index, the demand for longs is sustained by negative funding. This decreases demand for shorts in the market, and traders are inclined to call longs until the price approaches index.

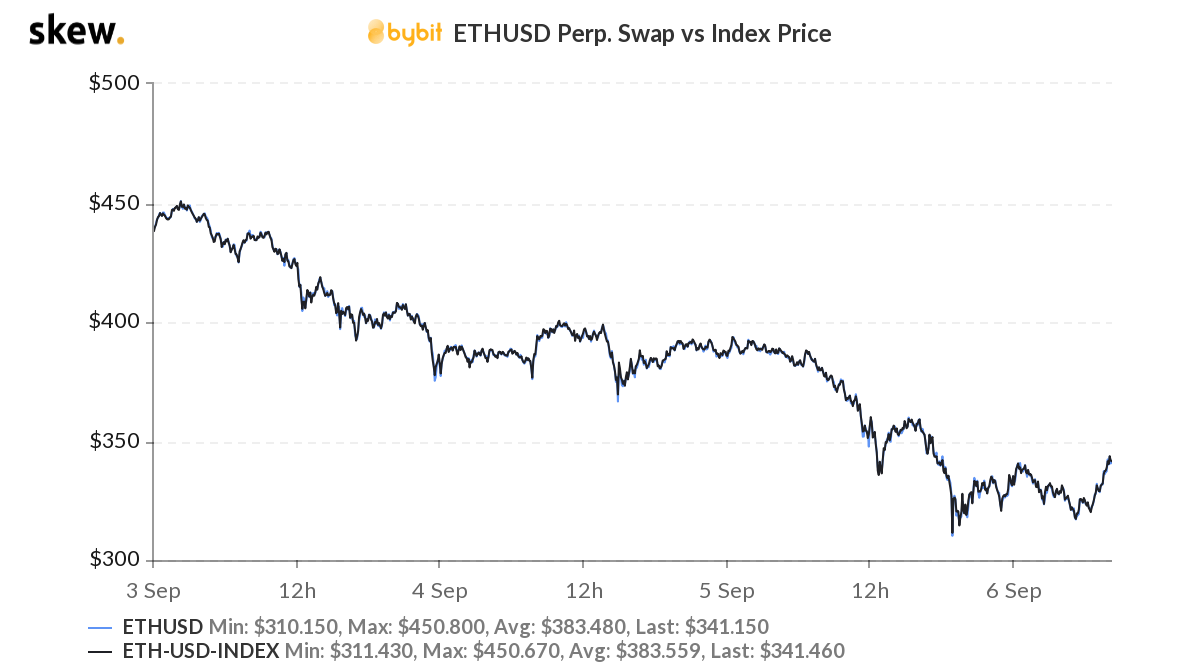

Currently, the ETHUSD perpetual swap v index price chart on Bybit seems to have seen better days.

Source: Skew

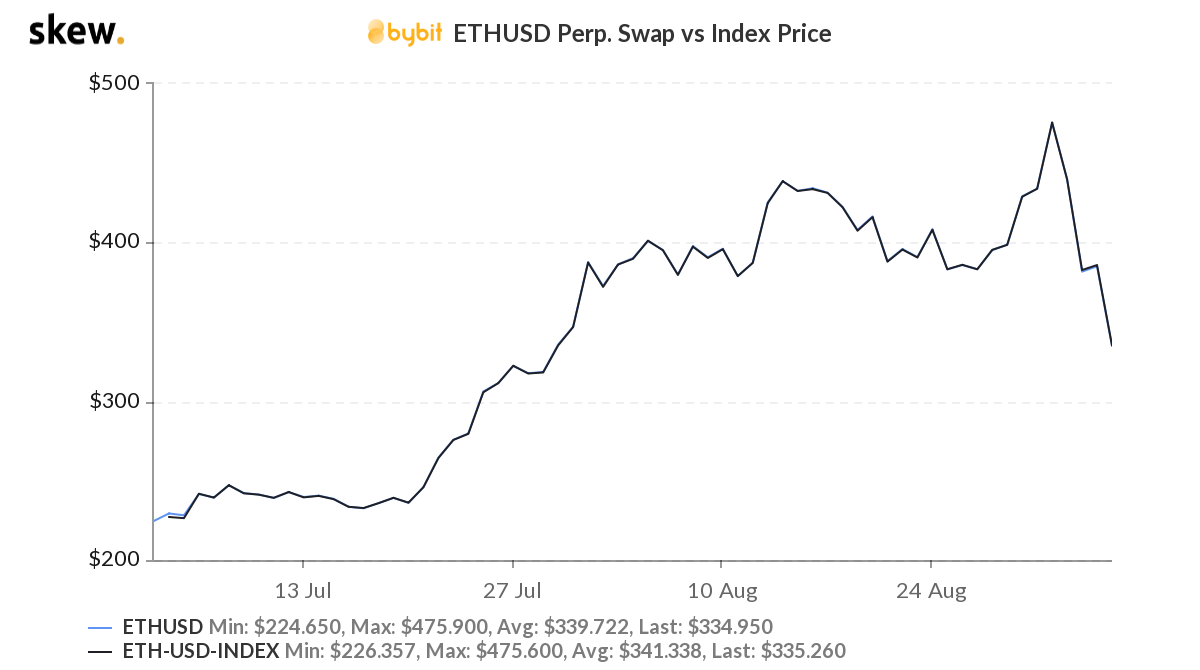

The 3-day chart showed a significant drop from $438 to $341. This drop of over 22% is not a positive sign for ETHUSD market. The performance in the past 3 months was better in comparison to the past 3 days. It was $475.6 on 1 September, up by $250 in the first week of July 2020, based on data from skew charts.

Source: Skew

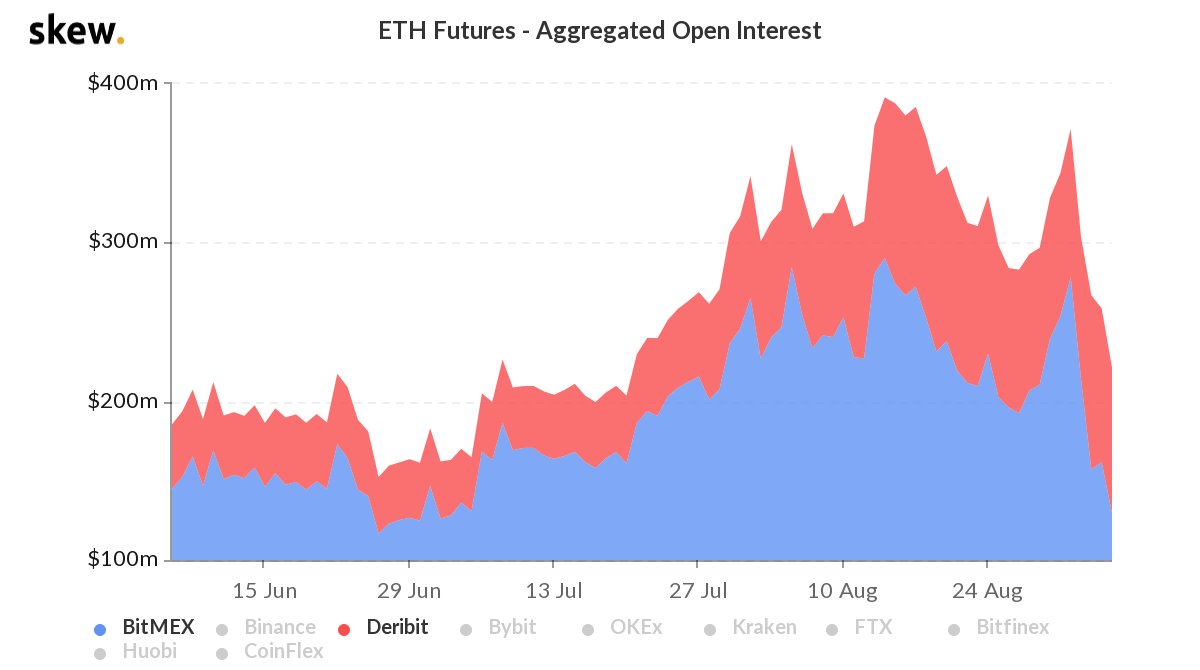

This exponential rise from early July can be attributed to the Defi boom and increase in the volume of open interest in Ether contracts on top derivatives exchanges. There was a higher number of long positions for ETHUSD before the recent drop in the perpetual swap. Another factor that follows the trend is ETHUSD open interest. Based on this open interest chart (below) for BitMEX and Deribit by skew, open interest was at its peak in the second week of August and the first week of September 2020. This corresponded with the performance of Perpetual swap v Index price on Bybit.

Source: Skew

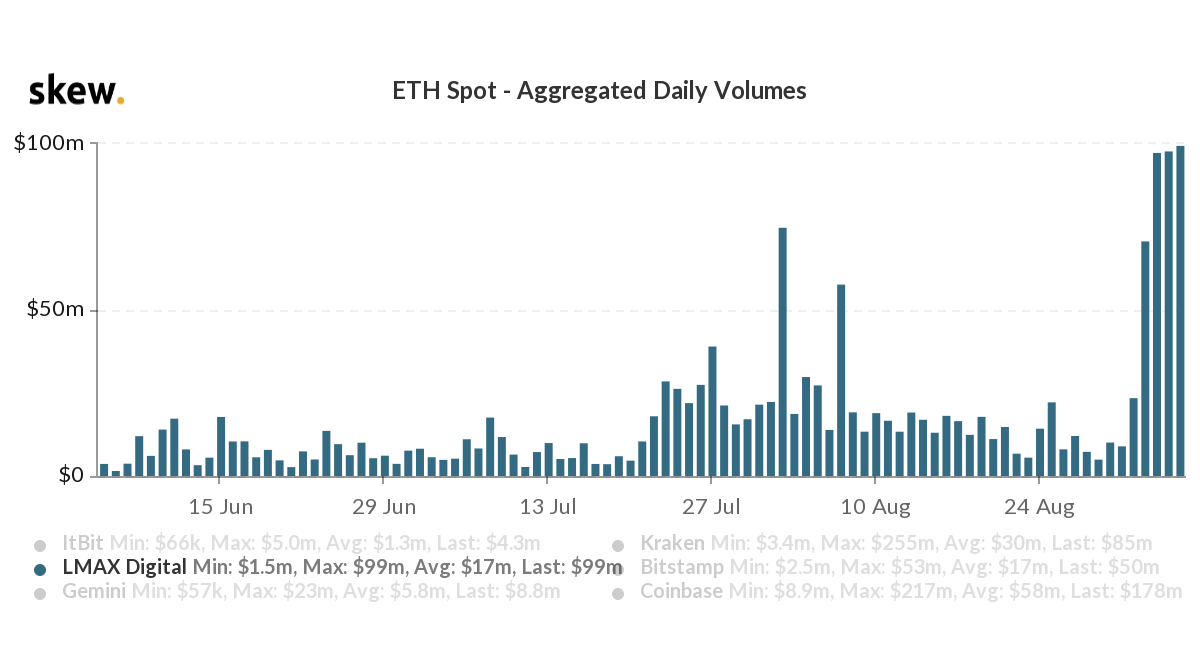

If open interest drops below $77M on Deribit, a free fall may follow and the perpetual swap chart will record a steeper drop in the following weeks of September 2020. Daily volume on spot exchanges is a factor that may have an inverse correlation with perpetual contract prices. There was a significant rise in daily volume on spot exchanges, LMAX Digital in particular, and this can be attributed to the drop in perpetual contract prices. To bring it closer to index price, there is an increase in trading activity on spot exchanges.

Source: Skew

Once the perpetual contract price approaches the next index price, there may be a drop in daily volumes. However, if it is sustained, this may signal a change in the perpetual contract price in the following weeks.